Most financial advice assumes you already have money. If you’re starting with $100, this guide is built for you which accounts to open, what to buy, how to save money consistently, and what mistakes quietly kill returns before they start.

Choose the Right Account Before Anything Else

The account type determines how much of your return you actually keep. This is where most beginners lose money without realizing it, not in the market, but at tax time.

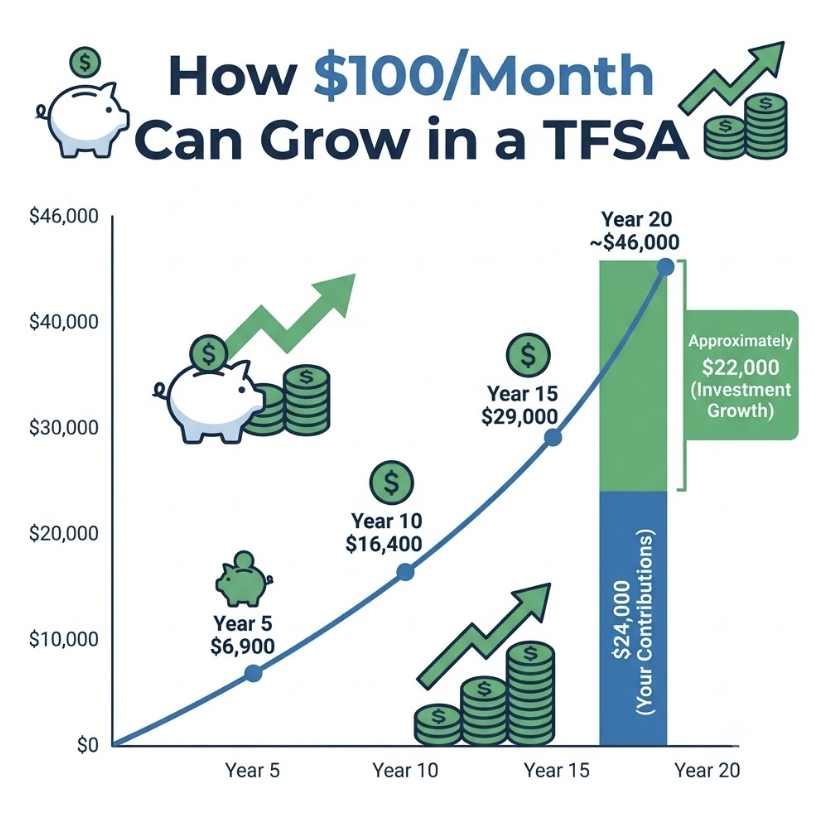

TFSA: The Default Starting Point

The Tax-Free Savings Account shelters all growth from tax capital gains, dividends, interest. Withdrawals are tax-free too, and any room you withdraw is restored the following January 1st. As of 2025, cumulative contribution room reaches $102,000 for Canadians who were 18 or older in 2009, according to the Canada Revenue Agency. Annual room for new investors is $7,000.

The TFSA wins for most beginners because it’s flexible. You’re not penalized for needing the money at 35, unlike an RRSP.

Platforms like 777Vault Casino show clearly how discretionary entertainment spending competes directly with investment capital. Those dollars can only go to one place.

RRSP and FHSA: When They Make Sense

RRSP: Contributions provide a tax deduction that’s particularly handy when your income climbs to a higher tax bracket. Withdrawals are taxed as income, so the strategy is for contributions to be made during high-earning years and then withdrawn during low-income retirement years. Maximum for 2024: $31,560 (18% of previous year’s earned income).

FHSA: If owning a home within the next 15 years appears to be in the cards, consider using the new FHSA. Like an RRSP, contributions are tax deductible. Withdrawals are tax-free if used for the purchase of a first home. Maximum annual contribution: $8,000. Lifetime limit: $40,000. It combines the best features of both registered accounts.

Where to Open the Account

Skip the major banks for your first investment account. Their mutual funds carry management expense ratios (MERs) of 1.5–2.5%, which cost roughly $1,000 per year on a $50,000 portfolio before you’ve earned anything.

Better options:

Wealthsimple Trade. No commissions on Canadian ETFs, fractional shares, no minimum deposit. The simplest starting point.

Questrade. ETF purchases are free; selling costs $4.95–$9.95. More tools, better for investors who want room to grow.

Wealthsimple Invest. Robo-advisor that builds and rebalances a diversified portfolio automatically. Fee: 0.5% annually. Ideal if picking ETFs feels overwhelming.

Opening any of these takes under 15 minutes online.

What to Buy With $100

ETFs: The Practical Default

A single ETF purchase gives you instant diversification across dozens or hundreds of securities. Three worth knowing:

XEQT (iShares Core Equity ETF Portfolio) — Global equities across Canada, US, international, and emerging markets in one ticker. MER: 0.20%. The closest thing to a set-it-and-forget-it equity position available to Canadian retail investors.

VCN (Vanguard FTSE Canada All Cap) — Canadian equities only, MER: 0.05%. Useful for a deliberate home-country tilt.

ZAG (BMO Aggregate Bond Index ETF) — Canadian investment-grade bonds, MER: 0.09%. Reduces volatility when paired with equity ETFs.

A simple starting point for most beginners: 100% XEQT inside a TFSA.

Dividend Investing: Income That Compounds

Dividend investing for beginners Canada carries a structural advantage: the dividend tax credit reduces the effective tax rate on eligible Canadian dividends received outside registered accounts. Inside a TFSA, everything is already sheltered, but dividend reinvestment still compounds effectively.

Three stocks with reliable dividend histories: Royal Bank of Canada (RY, ~3.5–4% yield), Fortis (FTS, ~4% yield, 50+ consecutive years of increases), and Enbridge (ENB, ~6–7% yield, higher payout ratio warrants monitoring). With fractional shares on Wealthsimple, you can hold a position in any of these with $100.

How to Save Money to Keep Investing

Knowing how to save money consistently matters more than picking the right ETF. A few methods that actually work:

Automate the contribution. Set a recurring transfer on payday even $25 directly into your TFSA. The FCAC consistently cites automation as one of the most effective behavioral tools for building long-term savings habits.

Redirect windfalls with a rule. The CRA issues average tax refunds of over $1,800 to Canadian filers. Without a standing rule, that money disappears into consumption. Decide in advance: “50% of any windfall goes to investments.”

Track savings rate, not just amount. A 5% savings rate on $40,000 income produces $2,000 annually enough to build a real portfolio over time. The dollar figure matters less than the consistency.

Risk, Time Horizon, and Common Mistakes

Money needed within three years doesn’t belong in equities. The TSX dropped roughly 37% during the 2008 financial crisis and took years to recover. Short-term capital belongs in a high-interest savings account inside a TFSA EQ Bank and Oaken Financial currently offer 4–5% annually.

For money untouched for ten years or more, equity ETFs have historically delivered meaningful return premiums over fixed income. A rough allocation framework: subtract your age from 110 to get your equity percentage. At 25, that’s 85% equities, 15% bonds. It’s a heuristic, not a rule but it grounds decisions in timeline rather than gut feeling.

Two mistakes that quietly erode returns: holding cash inside a TFSA without investing it (the account is a wrapper, not an investment), and checking the portfolio too frequently. Vanguard’s behavioral research consistently shows that investors who review less often make fewer costly decisions. Quarterly reviews are enough.

Conclusion

Open a TFSA on Wealthsimple or Questrade, transfer $100, buy XEQT or a comparable diversified ETF, and automate a monthly contribution. Review quarterly. Increase contributions as income allows.

The investors who build real wealth in Canada aren’t the ones who found the perfect stock. They’re the ones who started early, kept fees low, and didn’t stop when markets fell. That’s available to anyone with $100 and a browser.